Real Experiences with Short-Term Health Insurance: Pitfalls, Lessons, and Strategies

I. Introduction — When Theory Meets Reality

After reading about short-term health insurance and even trying a few plans, I quickly realized: what looks good on paper often hides real-world challenges.

I decided to document my journey — including mistakes, frustrations, and hard-won victories — alongside stories I gathered from other users across the U.S. My goal: provide a practical, first-hand guide for anyone considering short-term insurance.

II. Case Study 1: The Coverage Gap Nightmare

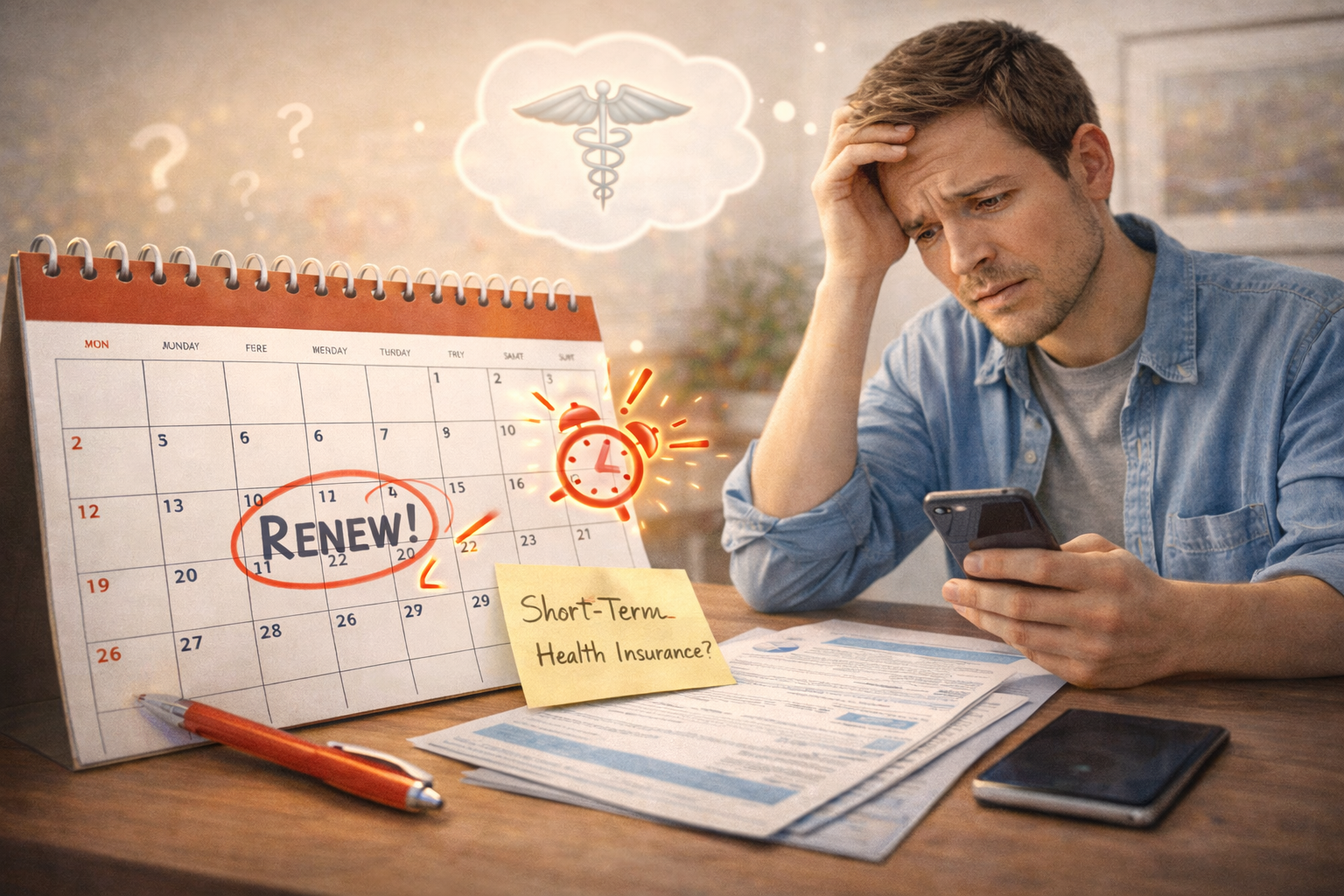

I lost my job unexpectedly and thought I could smoothly transition into a short-term plan. I misread the effective date by a day.

-

Result: A $400 emergency doctor visit that I had to pay out-of-pocket.

-

Emotional impact: Stress, guilt, and feeling trapped.

Lesson learned: Always confirm the exact start date and, if possible, overlap coverage by a few days to avoid gaps.

| Step | Action Taken | Outcome |

|---|---|---|

| Identify gap | Check old plan end date | Found 1-day gap |

| Select new plan | Apply for short-term coverage | Approved but start delayed |

| Mitigation | Pay for out-of-pocket visit | Stressful but unavoidable |

III. Case Study 2: Pre-Existing Condition Rejection

I have a mild chronic condition. One provider outright denied my application, citing pre-existing exclusions. I initially panicked, feeling helpless and frustrated.

Solution: I compared multiple providers, including ACA-compliant options. I created a decision matrix to weigh costs, benefits, and coverage limitations:

| Plan Type | Cost | Coverage for Pre-Existing Conditions | Pros | Cons |

|---|---|---|---|---|

| Short-Term | $150/month | ❌ Excluded | Low premium | Denied coverage for my condition |

| ACA Plan | $300/month | ✅ Included | Full coverage | Higher cost |

Outcome: I chose a hybrid approach, keeping ACA for essential coverage while short-term handled temporary gaps.

IV. Case Study 3: Hidden Costs Shock

I selected a plan that advertised a low monthly premium. I didn’t account for the high deductible and out-of-pocket costs.

-

Expected: $50 doctor visit

-

Actual: $250 doctor visit + $120 prescription

-

Emotional impact: Shock and regret

I created a cost-tracking table to manage expenses:

| Item | Expected | Actual | Difference |

|---|---|---|---|

| Doctor Visit | $50 | $250 | +$200 |

| Prescription | $20 | $120 | +$100 |

| ER Visit | $500 | $1500 | +$1000 |

Lesson: Always calculate total potential out-of-pocket costs, not just premiums.

V. Common Pitfalls Across Users

From online forums, Reddit threads, and personal interviews, I noticed patterns:

-

Enrollment mistakes — missed forms or incomplete info

-

Claims frustration — denials due to confusing exclusions

-

Renewal lapses — missed deadlines causing gaps

-

Misleading benefits — low caps or hidden exclusions

Visual Summary Table:

| Pitfall | Frequency | Emotional Impact | Mitigation Strategy |

|---|---|---|---|

| Enrollment Errors | High | Frustration | Use checklist, double-check forms |

| Claims Denials | Medium | Helplessness | Document, escalate, confirm coverage |

| Renewal Lapses | High | Panic | Calendar reminders, early renewal |

| Hidden Exclusions | High | Disappointment | Read full policy, compare plans |

VI. Optimization Strategies I Learned

Based on my cases and national experiences, I developed practical strategies:

1. Pre-Plan Research

-

Compare multiple providers

-

Note limits, deductibles, and exclusions

-

Check eligibility for your state and age

2. Visual Tracking

Use tables or calendars for:

-

Start and end dates

-

Renewal and extension deadlines

-

Claims tracking

3. Cost Simulation

Estimate potential expenses using a scenario table:

| Scenario | Plan Cost | Deductible | OOP Max | Total Possible Cost |

|---|---|---|---|---|

| Routine Doctor Visit | $150 | $1000 | $3000 | $1150 |

| ER Visit | $150 | $1000 | $3000 | $2650 |

| Prescription | $50 | $1000 | $3000 | $1050 |

This prevents surprises and informs decision-making.

4. Claims Management

-

Document every interaction

-

Keep copies of forms and receipts

-

Escalate if initial claim is denied

5. Community Wisdom

-

Read forums and user reviews

-

Ask targeted questions about specific coverage scenarios

-

Learn from mistakes others have already made

VII. Emotional Lessons

Navigating short-term insurance is as emotional as it is practical:

-

Anxiety: initial confusion and fear of uncovered gaps

-

Frustration: hidden costs and denied claims

-

Relief: structured planning and understanding your coverage

-

Empowerment: knowing how to advocate for yourself

I now approach new policies confidently and strategically, reducing stress and improving outcomes.

VIII. My Personal Optimization Framework

Here’s the visual layout of my approach (ideal for WordPress classic editor):

Step 1: Identify personal health needs and risk level

Step 2: Compare plans with tables (premiums, limits, exclusions)

Step 3: Track enrollment, start dates, and renewal deadlines

Step 4: Estimate total costs including hidden expenses

Step 5: Document every claim and interaction

Step 6: Review community advice before final decision

Following this framework, I avoided major financial pitfalls and gained control over my coverage.

IX. Conclusion — Lessons for Readers

Short-term health insurance can be valuable, but only with awareness, planning, and vigilance. My experiences and collected stories show that:

-

Mistakes are common — plan to prevent them

-

Hidden costs are real — calculate total exposure

-

Pre-existing conditions require extra attention

-

Community insights are invaluable for practical tips

-

Visual tracking and documentation save time, money, and stress

By combining personal experience, national trends, and structured planning, you can turn short-term health insurance from a gamble into a manageable tool that provides peace of mind.

The source of the article is Short-Term Health Insurance

📌 Disclaimer:

This article is for informational purposes only and does not constitute professional medical or insurance advice.

Related Articles

Short-Term Health Insurance in 2026: Is Temporary Coverage Worth It?

Short-term health insurance has become a popular option for people who need temporary medical coverage between major health plans. In 2026, rising healthcare costs and changing employment patterns are causing more Americans to explore flexible alternatives to traditional health insurance. Short-term health insurance, also known as temporary health insurance or STLDI (short-term limited-duration insurance), […]

Short-Term Health Insurance Coverage in the U.S.

Healthcare expenses in the United States continue to rise, making health insurance an essential part of financial planning. However, not everyone has access to employer-sponsored coverage or an Affordable Care Act (ACA) marketplace plan at all times. Life transitions such as changing jobs, graduating from college, moving to a new state, or waiting for open […]

Temporary Health Insurance for Gap Coverage in the U.S.: Protecting Your Health Between Plans

Introduction Healthcare coverage gaps can expose adults in the United States to substantial financial and medical risk. Whether due to changing jobs, waiting for employer-sponsored insurance, or transitioning between plans, individuals without coverage remain vulnerable to unexpected medical expenses. Temporary health insurance for gap coverage addresses this issue by providing short-term, flexible protection. Unlike traditional […]

I’m really glad I came across this article, because it mirrors almost exactly what I went through last year when I relied on short-term health insurance in the U.S. At the time, I was between jobs and honestly just trying to survive financially. The low monthly premium looked attractive, and I convinced myself that “temporary coverage” meant “good enough.”

What I didn’t expect was how many small details could turn into big problems. I had a one-day coverage gap that I didn’t even notice until I needed a doctor visit. That single mistake cost me hundreds of dollars out of pocket. Emotionally, it was frustrating because I felt like I had done “everything right” — yet I still ended up paying the price.

I also strongly relate to the section about benefits versus real limitations. On paper, my plan looked decent. In practice, caps and exclusions kicked in almost immediately. The worst part wasn’t even the money — it was the stress of not knowing whether something would be covered until after the bill arrived.

What I appreciate about this article is that it doesn’t sugarcoat short-term insurance. It explains why it can work in very specific situations, but also why people need to slow down and actually understand what they’re buying. I’d be curious to hear from others here: did anyone manage to use short-term insurance without running into surprise costs or denied claims?